General Description

Mid America Mortgage’s Down Payment Assistance Program provides the first mortgage financing and down payment/closing cost assistance to eligible mortgagors and low to middle income borrowers in conjunction with Freddie Mac’s Home Possible product. The down payment/closing cost assistance is in the form of a second mortgage to the borrower which is forgivable after five years. The program is created to provide housing opportunities to low to moderate income individuals and families. This is available for Government loans.

Setting up the Rosebud Program in Mortgage Machine

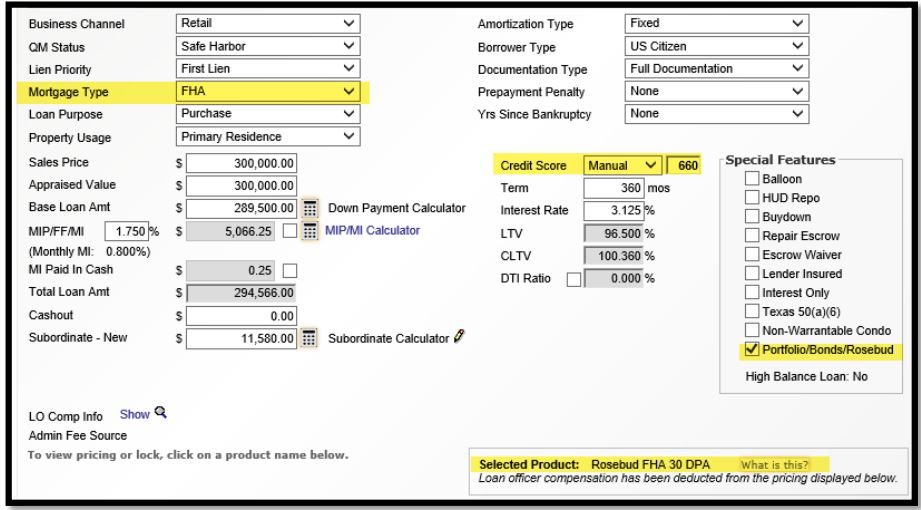

Once you create your lead in Mortgage Machine you will go to your Pricing & Borrowers page and choose the Rosebud Program.

You are going to check mark “Portfolio/Bonds/Rosebud” in Special Features.

Once you have entered all the information you will save and then the product will appear.

You want to make sure your borrower meets all regulations or the program may not appear.

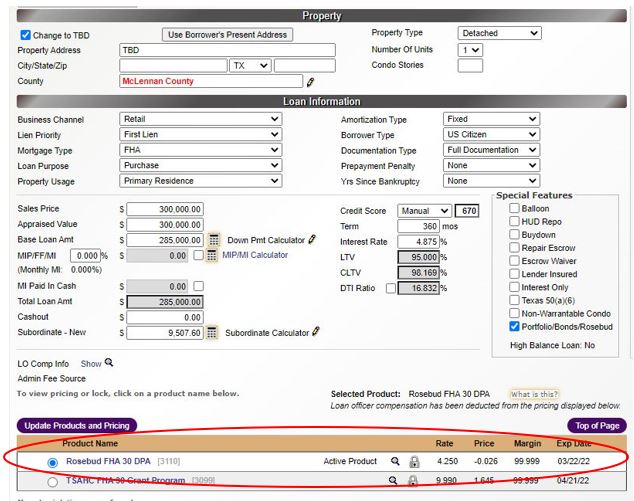

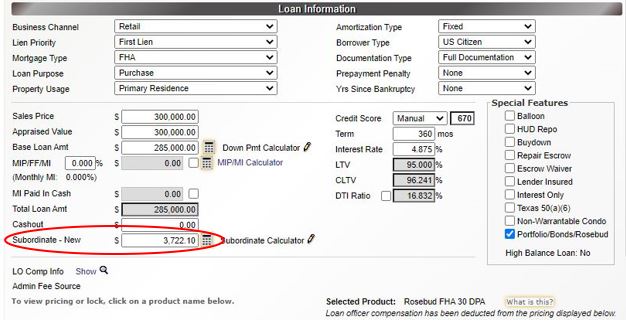

Once you choose the Rosebud program it will take you to the Pricing Sheet and this is where you will be able to choose the rate you want your borrower to have.

When you click on the rate you want you will need to keep note of the Discount Points that you choose. These numbers are the amount (%) that the borrower was approved based on the product you chose. Keep in mind that when looking at these numbers you want to make sure you choose the highest (-) number that the borrower was approved.

Discount: Number is positive; this means that we will be charging the borrower this percentage of the Base Loan Amount.

Points: Number is negative; this means that we will be giving them this percentage amount of the Base Loan Amount.

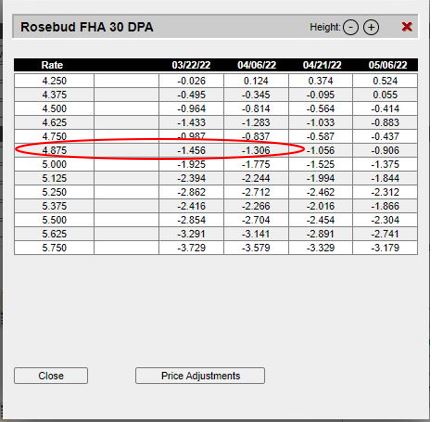

In this example we will be choosing the rate of 4.875 with a Point (%) of -1.306.

You will want to keep note of the Discount Points that you choose, you will need this for later.

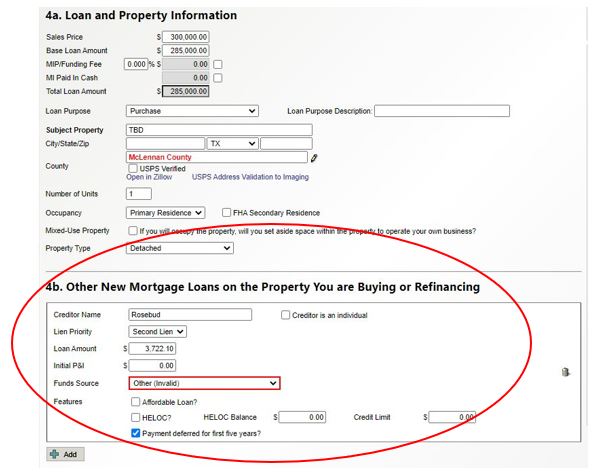

Once you choose the Rosebud program you will want to click on Loan/Property and add the program here.

You will click on Add on the 4b. section in order to add the Rosebud program. The following is everything you need to add to this section.

Creditor Name: Rosebud

Lien Priority: Second Lien

Loan Amount: This number you will get by multiplying the Discount Points that the borrower was approved by the Total Loan Amount.

Discount Points x Base Loan Amount = Loan Amount

- In this example, we would multiply the following – 1.306% x $285,000 = $3,722.10

- This means that we will be giving the borrower $3,722.10 as part of the Second Lien.

Initial P&I: 0.00

Funds Source: Other

Features: You will want to make sure that you check mark “Payment deferred for first five years?”

You will then want to go back to your Pricing & Borrowers page and add the Loan Amount in the Subordinate – New section.

Qualifying Guidelines

Terms and Schedule

The down payment assistance is in the form of a second mortgage forgiven if the first 60 payments on the first mortgage are made timely. Timely is considered zero 90-day late payments.

The second mortgage will be a five-year loan with no interest and no payments.

At the close of year five the full and total principal amount is forgiven.

If the first mortgage is paid off via a purchase or refinance within the first five years, the full amount of the DPA will be required to be paid back.

Eligible Lenders

Lenders must be approved by MAM. Interested lenders should contact their Account Executive.

Third Party Originators are accepted. MAM lender must have previously received TPO approval and be in good standing with MAM. Any TPO’s on a watch list or under heightened quality control review are not eligible until removed from either the list or the heightened review.`

Loan Purchase

MAM will close the first mortgage loan at a rate and price reflected on the lock reflected in Mortgage Machine, less any fees charges.

Third party originators Lenders

Types of Loans

FHA, USDA, and HUD-184 purchases and no cash-out loans on a primary residence. Rosebud cannot be used with VA loans.

Eligible & Non-Eligible Properties

Eligible: 1-Unit

Non-Eligible: 2+ Units, Co-ops, Manufactured Homes, Log Homes, Bamboo Homes, Metal Homes, Container Homes, and Post-Frame Homes

Occupancy Type

Must be owner-occupied.

If the property is later moved to an investment property in the first five years, the full amount of the DPA will be required to be paid back.

Maximum Loan Amounts

Amount of assistance is 2.0% to 6.0% of the base loan amount.

While, MAM will allow up to 6% of the total loan amount, the TPO may cap it below the max allowance. Mortgage Machine will round to the nearest dollar.

Funds Use

The funds may be used to fund up to 100% of the Borrower’s cash requirement to close including

- The down payment

- Closing costs

- Pre-paid items

- Any other related Mortgage Loan fees and expenses

AUS Eligibility

Loans may be underwritten through Mortgage Machine utilizing DU, LP, GUS. If the loan is underwritten outside of Mortgage Machine, it must still go through an approved AUS (i.e. DU, LP, GUS). Loans are not eligible for manual underwrite with the exception of Mid America Mortgage’s HUD-184 loans.

Allowable & Required Fees

Standard fees normally charged to the borrower will apply for the first mortgage – no other fees may be added as a result of the DPA program.

No fees are permitted on the second/DPA program. The only fee associated with the Rosebud DPA is the $500 REDCO fee which is to be charged on the first mortgage.

Borrower Eligibility

Borrower(s) does not have to be a First-Time Homebuyer. MAM has an overlay guide which should be referenced to determine the eligibility for the First Mortgage Program and, the DPA eligibility.

Non-occupying co-signers are permitted. They must have in excess of 5 monthly payments of the first mortgage’s PITI in reserve after closing for their income to be considered.

Payment shock will be taken under consideration – those greater than 50% will have a review of the Bank Statements and other compensating factors.

Credit Scores

Minimum Score of 640

Debt Ratios and Income

DTI will primarily be determined by the First Mortgage Program but should not ever exceed 55%.

- FICO scores between 640-649, the DTI cap is 45%

- FICO scores between 650-679, the DTI cap is 50%

- FICO scores greater than 680, the DTI cap is 55%

Homeownership Counseling

All DPA loans under this program are required to take Homeownership Counseling from a HUD approved or Housing Finance Agencies (HFA) approved course.

In the event the primary mortgage program does not require and dictate the counseling, all qualifying borrowers must take a Homeownership Counseling class with certificate. A certificate of completion will be required from all borrowers on the note. Borrower must agree to life of loan credit counseling.

Responsibility and General Flow

Correspondent Lenders must fund the First Mortgage Loans at loan closing. All loans will be locked, approved, DPA funds requested, and post-closing documents uploaded through Mortgage Machine. The Rosebud Sioux second mortgage will be considered locked simultaneously with the first mortgage when utilizing the Rosebud product in Mortgage Machine.

MCC Only Submissions

Submissions to underwriting for the MCC only programs will require three years of tax returns to ensure the borrower(s) qualify for the MCC Tax Credit.

Locking and Approval of DPA

When locking the first mortgage loan, the DPA amount will need to be manually deducted from

the overage of the lock.

Odd amounts can be used, as long as the amount stays within 2% to 6% of the base loan amount.

Overages are not to be kept by the branch, division, or TPO. The overage should be given to the borrower up to 6% of the base loan amount.

Closing and Funding the DPA

All closing documents and closing disclosures must be prepared through Mortgage Machine and electronically closed except for notes required to be papered.

A second loan will NOT need to be set up in Mortgage Machine. Closing will be able to draw both the first and second from the first mortgage information.

Rosebud - Blended Credit Score Feature

Eligibility

FHA & USDA Rosebud Products

How does it work?

- Does the higher wage earner have a better credit score? GREAT

- We can now blend the higher wage earner middle credit score with the lower wage earners middle credit

score to get a blended qualifying score of 660 or above.

Required

- The higher wage earner must have the higher credit score.

- There is no minimum credit score for the lower wage earner, as long as the blended score is 660.

- Must maintain AUS approval.

- All other Rosebud guidelines apply

Definition of Higher Wage Earner

- 60% or more of all household income for all borrowers on the application.

- Household income includes all income from each borrower on the loan application, even if the income is not

needed to qualify.

Calculating Blended Score Examples

Example 1:

- Primary Wage Earner – 751 760 761

- Secondary Wage Earner/Unemployed – 600 603 610

- Blended Score = 760 + 603 =1363 /2 = 681 Qualifying Score (Always Round Down)

This loan DOES qualify; the blended score is above 660.

Example 2:

- Primary Wage Earner – 600 603 610

- Secondary Wage Earner/Unemployed – 751 760 761

This loan does NOT qualify; the primary wage earner does not have the higher scores.

Example 3:

- Primary Wage Earner – 680 670 660

- Secondary Wage Earner/Unemployed – 600 603 610

- Blended Score = 670 + 603 =1273/2 = 636 Qualifying Score (Always Round Down)

The loan does NOT qualify; the blended score is below 660.

How to Price this Loan

- Use the Manuel Feature on the Pricing Page in Mortgage Machine to input the Blended Score

- The Blended Score will be used for pricing