CORE Principal Rick Ruby's Money Formula

Rick believes you should distribute your money as follows:

- 20% savings

- 10% giving

- 40% taxes

- 30% to live off of

Get a will, trust (update trust every 2 years) and $1M insurance umbrella. Life insurance: 30 year term until 50 years old/5-20x your income.

Before age 50, do not pre-pay on your mortgage.

Pay Bills Once a Month

In order to handle your money only once per month, you may need to change the billing date of some of your bills to the beginning of the month. Your mortgage is your most important bill. It’s due on the first, so that’s when you want to pay all your other bills.

Throughout each month, save all checks you receive in a drawer and save all bills you receive in a drawer. At the first of the month, deposit the checks, pay all your bills, allocate the rest of the money and fill out your budget.

This should be your mindset – on the 1st I’m rich; on the 2nd I’m poor and need to prospect.

Option #1 - Using Credit Cards

You want 2 Credit Cards: 1 card for business, 1 card for personal. You want the cards to have low limits, so you don’t get excessive with your spending.

- Every month, give yourself a $200 cash allowance. Purchases you make under $20, use cash. The biggest challenge of this option is NOT overspending. Once you use your $200, you can’t take money out of savings.

- Purchases above $20, put on the card.

If you use this option, you MUST pay your credit card off every month.

We don’t want you to have a ton of credit cards. A ton of credit cards usually equates to a ton of debt. So start paying that debt off, the smallest debt first. If you need to cut them up to avoid racking up more debt, do it!

Option #2 - The Envelope System

If you’re paying off credit card debt, use the envelope system instead. Once you paid your bills, allocate cash to the other categories that you spend money on throughout the month into envelopes (gas, groceries, entertainment, etc.)

Once the money in a certain envelope is gone, it’s gone. You can no longer purchase anything for that category until the next month. You will get better in time at allocating the right amount for each envelope and in the process, learn to limit your spending.

6 Rules of Money

- Fill out a personal family budget every month

- Save 20% of your gross income monthly (if you are unable to do 20% then pick a number and consistently stick to it)

- Have at least 3 months of your survival number in a savings account

- All of your 20% of savings goes into retirement accounts first

- Pay down debts with anything above and beyond your 20% in savings

- Buy things with future earnings (don’t spend with money you have already saved)

Pull the Trigger

In instances where you have already decided to perform an action, for example buying stock, do not wait in hopes that the prices will lower. Even during a dip in the market, if you plan to buy a certain stock, do not continue to wait for it to drop. If you make the decision to do it, then do it.

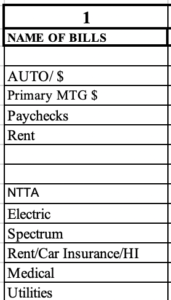

Column 1 - Name of Bills

The beauty of this form is it is editable! You can customize it to your life.

You need to put the balance of your home, car, and credit cards all in column 1.

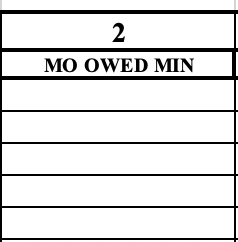

Column 2 - Monthly Owed Minimum

In column 2, you’re going to write the minimum amount owed.

Example: If you have an $8,000 credit card balance; but a $75 minimum payment every month– you’re going to write “$75” in column 2; even if you’ve paid more off. (Stay tuned for column 3).

You will not put things in column 2 that are one-time expenses; like an automobile repair or a vacation.

You will include things you pay for on a monthly basis. This isn’t just the bare essentials; it’s whatever it takes to keep up your lifestyle. If you are in a country club which has monthly dues, that will go in column 2. You’ll also include your spending money there.

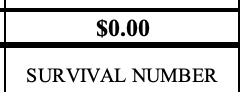

To get your survival number, you’re going to add all of the numbers in column 2. Again, this is not just what you need to survive. It’s just what it takes to be you every month.

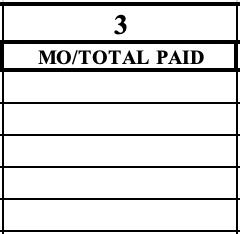

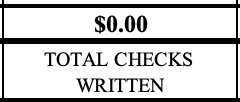

Column 3 - Monthly Total Paid

This is where you’re going to put how much you actually paid. This column is where you’re going to put one time expenses, like vacations, repairs, special expenses, etc.

So if your CC bill was $8,000 and you paid it all off, you’re going to put “8,000” on column 3; even if the minimum owed in column 2 was $75.

We always encourage you to pay off your debt with any extra money you have each month.

Rick advises that you pay off the card with the smallest balance first.

Always remember to add the total and put it in the area above Total Checks Written.

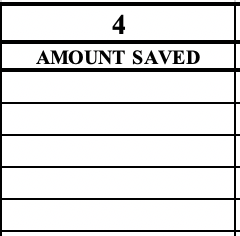

Column 4 - Amount Saved

Exciting news! If you pay down any debt, that counts as savings. So if you have CC debt of $8,000 with a minimum payment of $75, and you actually pay $8,000– Rick Ruby says you’ve saved $7,925! (ONLY if you’re not using that card for spending. If you are just paying off what you spent that month, it is not savings).

If you’re in a 401k program or IRA, that will go directly into column 4. It should not go in column 3 since it is taken out pre-tax.

Make sure you add up your savings and put them in the space above Total Monthly Saved.

If you pay extra on your home or car, it counts as savings. Life insurance does not count as savings

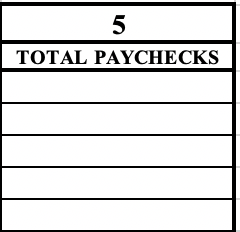

Column 5 - Total Paychecks

This is where you put all of the money coming in for the month, and where it’s coming from.

Always remember to add up your paychecks/any income you receive and put it in the space above Net Income for Month.

Label all checks received.

If they had to take money from savings, show that in column 5 as income “from savings”. Do not put negative savings on the budget. You either save money or saved $0.

Column 3 and Column 5 are ALWAYS going to match

If they’re not matching- it’s not correct!

Any money left over after you’ve paid your bills needs to be allocated somewhere. It can be to giving, saving, paying down debt, etc. Decide how to allocate the money and indicate that in column 3.

If they don’t match, you’re not following the process, or there’s money left in your checking account. If you follow our system, you won’t have any money in your checking account; and column 3 and column 5 will match.

Bottom Section

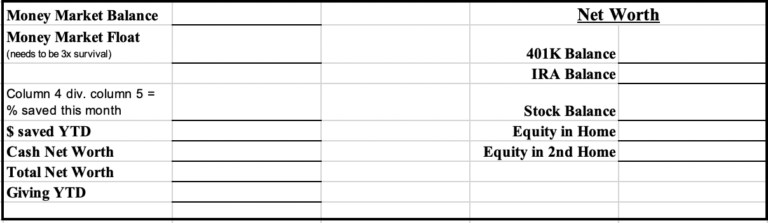

Money Market Balance

- The Money Market Balance is the amount you have in your savings or money market account.

- If you have more than your survival number, it’s time to invest!

- Invest in chunks, not all at once

- If you have under $500K, invest in mutual funds

- If you have over $500K, invest in mutual funds, stocks and index funds

Money Market Float

- Your Money Market Float needs to be 3X your survival number (from column 2). We want you to save 3X your survival number because if something happens (medically, family emergencies, car emergencies, job changes); we want you to be covered for three months.

- Once you’ve reached 3X your survival number, you’re going to start investing & putting money in 401k.

- If you have debt and no float, then you need to start putting half of your extra money toward each every month. So build the float while paying down debt. ½ the money toward float account and ½ the money toward debt.

Column 4 Divided by Column 5 Equals % Saved This Month

- To get the right % for “Column 4 div. Column 5 equals % saved this month” take the number above Total Monthly Saved in column 4, and divide it by the number above Net Income for Month.

- The CORE Trains that you should save at least 20% of your paycheck every month.

$ YTD Saved

- Go through your Personal Family Budget and look at the number above Total Monthly Saved; add them up for the year to find your $ YTD Saved.

- If you haven’t kept track of your savings yet, don’t worry. You’re going to start now.

Cash Net Worth

- Your Cash Net Worth comes from your money market balance + savings + 401K + stocks.

- The longer you do the Personal Family Budget and follow The CORE financial plan, the more core CNW will grow and strengthen.

Total Net Worth

- You can get your Total Net Worth by adding your equity in home and rentals to your CNW.

Giving YTD

- The CORE Training’s mission is to make the world a better place. We consistently donate to charities and volunteer our time to causes we love. We want you to give away 10% of what you bring in every month.

- Give monthly, not yearly. Give to 3-4 places every month

- “If you want a fun and highly profitable company, you have to be more grateful and generous.”

- In a bad month, be more generous!

401K Balance

- You’re going to put your 401K Balance here

- If you’ve hit your Money Market Float, you should get started in a 401K plan

Mutual Fund Balance

- If you’ve chosen to invest in a Mutual Fund, this is where you would put that balance

- Rick Ruby says if you’ve hit your Money Market Float and you’re involved in a 401K, you should either invest your extra money every month in a Mutual Fund or in the Stock Market

Stock Balance

- If you’ve chosen to invest in the Stock Market, this is where you’ll put the balance.

- Investing in the Stock Market or in a Mutual Fund will grow your finances even more

Equity in Home and Rentals

- This is where you’re going to put the equity in your home(s), and rental properties

- The formula for finding the equity in your home is: (Amount your house is worth minus How much you owe)